Within a screened, borrowing-relevant audience of US adults, 65% owned digital assets, more than double the 25% national ownership rate reported by The Harris Poll in 2026. And after reading a plain-language description of a collateral-enabled loan Vault's infrastructure enables for consumer lenders, 85% said they would consider one from a trusted lender. Those are the headline results of a concept-validation study we commissioned from PinPoint Collective, a market research firm, fielded in May 2026.

This article covers what we asked, what we found across ownership, borrowing behavior, concept reaction, and trust, and what it means if you run a consumer lending book.

Why we ran the study

Vault's value proposition for borrowers is the ability to use liquid financial assets to secure better credit terms on consumer loans. "Better credit" could mean access to credit at all, or more favorable terms, a lower rate or a larger loan, than the applicant's FICO score and income alone would justify. Our longer-term vision is to support all types of liquid financial assets; today, we support Bitcoin and Ethereum.

Lenders overwhelmingly see the benefits, but inevitably ask the same follow-up: "This makes sense, but how many of my target borrowers actually own digital assets? And how do you know they would pledge them?"

These are exactly the right questions. National surveys speak to a borrower's ability to participate, but not to their willingness or to the ownership rate among the credit-seeking adults lenders actually target. So we designed the study around both.

How the study worked

The structure matters for reading everything below, so here it is in one line: 600 screened, 388 owners, 60 qualified.

We started with a screened pool of 600 US adults. The screeners were simple: aged 25 to 50, with a household income of $60,000 or more, and employed or in school. That is a much closer approximation of the applicants that most lenders target than a general-population sample. Within that pool, 388 respondents, or 65%, owned digital assets. From those crypto owners, we selected 60 respondents who had also actively sought or explored credit in the prior two years, and this group answered detailed questions on borrowing, the concept, and trust.

The qualified group skews toward prime borrowing ages (58% were 35 to 44), is financially established (78% reported household income between $80,000 and $150,000, and another 12% above $150,000), and is 63% men and 37% women.

Two call-outs. First, the findings are directional, given the sample size. Second, a screened online panel of younger, financially established adults would be expected to over-index on financial engagement relative to the general population, which is consistent with the elevated ownership rate. The value of the study is the signal within the audience lenders actually reach, not a new national estimate.

Ownership is real, and it sits on mainstream rails

The 65% ownership rate was well above what national surveys implied, and the holdings behind it are substantial enough to matter. Among the 388 owners in the screened pool, 52% held $1,500 or more in crypto. Storage skewed to mainstream venues: crypto exchanges were the most common place assets were held, followed by mobile wallet apps, then hardware wallets and investing apps.

Among the 60 qualified respondents, the asset mix concentrated in exactly the assets a collateral program supports: 90% held Bitcoin, 62% held Ethereum, and 68% said the majority of their holdings sat in Bitcoin.

This group is also hands-on with their assets. Of the qualified respondents, 93% said they are the primary decision-maker for their crypto, 82% had already moved assets between wallets, platforms, or accounts, and 80% said they were at least somewhat comfortable doing so. Transferring crypto into a custody account is not a foreign behavior for this audience. The friction to solve is trust and clarity, not basic fluency.

These borrowers are active and often dissatisfied

Because we screened for recent credit seekers, their reactions are grounded in actual borrowing rather than hypothetical intent. In the prior 12 months, they had explored or applied across multiple products: credit cards (66%), personal loans (52%), auto loans (45%), and mortgages (35%) led the list.

Their borrowing experience often fell short. Nearly half (48%) were dissatisfied with some aspect of their most recent loan search. Forty-seven percent were approved, but at a rate, term, or amount below what they wanted. Thirteen percent walked away because the terms did not seem worth it, and 5% were denied outright.

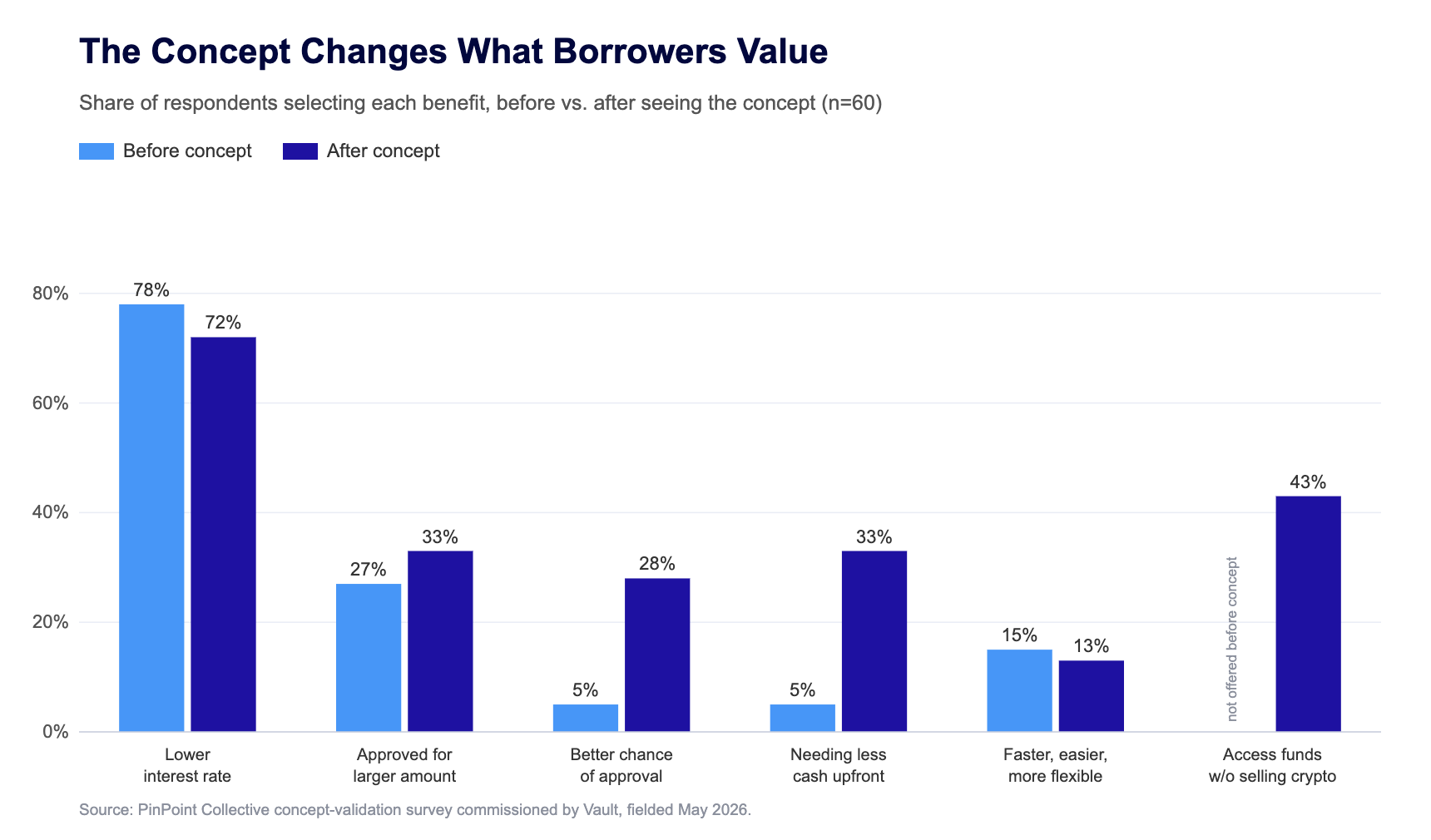

When we asked what would have made the experience meaningfully better, one answer dominated: 78% pointed to a lower interest rate, well ahead of a larger amount (27%), a faster process (15%), or more flexibility in qualification (13%). The single biggest source of borrowing friction is precisely the lever on which collateral is expected to move.

The Vault concept resonates, and the appeal is specific

We then showed respondents a plain-language description of the concept: a loan from a lender you trust that lets you pledge roughly 10 to 15% of the requested loan amount in crypto, held by a qualified custodian, with no margin calls or forced liquidations, and with the assets returned upon full repayment.

After reading it, 85% said they would consider a loan that lets them pledge crypto for better terms. 35% were extremely interested in the concept.

Lower rates carried the appeal both before and after the concept was introduced. Asked to pick the single most compelling benefit, 53% chose a lower interest rate, followed by access to funds without selling crypto (22%). Just as interesting is what the concept unlocked: benefits that had been abstract on their own jumped once respondents saw how the mechanics would deliver them. A better chance of approval went from 5% to 28%, the need for less cash upfront went from 5% to 33%, and access to funds without selling, which was not on the radar before the concept, was selected by 43% after.

Respondents also gave us thresholds for what would make each benefit worth it, which is where the smaller bases come in. Of the 43 who cited lower rates, 28% said a reduction of 1 to 2 percentage points would be enough to make the concept worth considering, with the rest wanting more. Of the 21 who cited access to funds without selling, the main motivations were avoiding the sale of crypto they expect to appreciate (39%) and avoiding the tax consequences of selling (35%). Two use cases drew unusually strong, if small-sample, signals: of the 17 who cared about a second chance at approval, 65% said that alone could make the concept worth considering, and of the 20 who cared about down-payment support, every one said using crypto instead of cash toward a car or home down payment would be worth considering. Treat those last two as directional, given the bases, but they point squarely at "second look" and a cash down-payment alternative as high-intent entry points.

Trust hinges on mechanics, not just brand

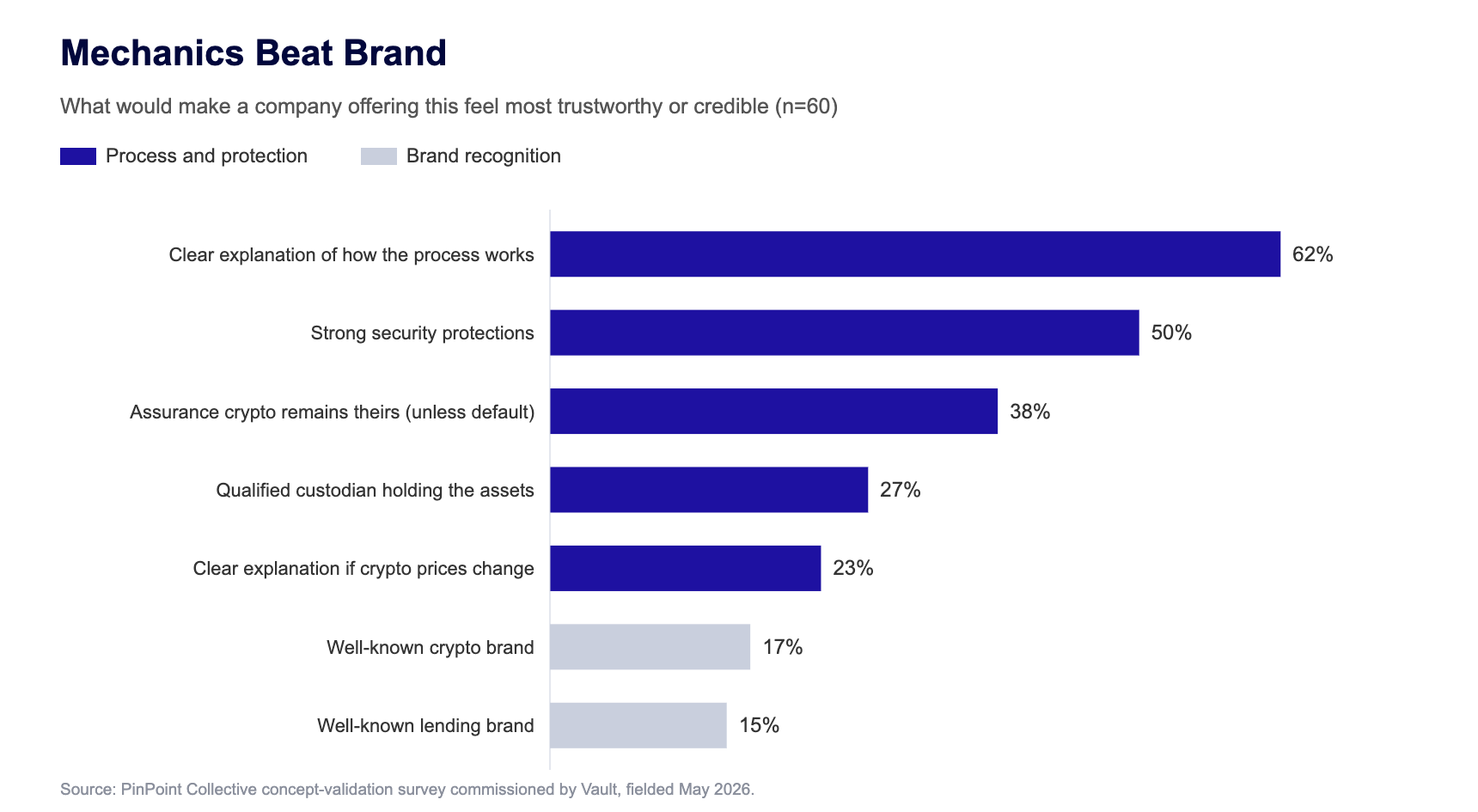

The most important finding for how a lender rolls this out: comfort with the core mechanics was already high, and what moves people from interested to comfortable is clarity, not a famous logo.

Ninety-three percent were comfortable working with a lender that partners with a crypto platform, 90% were comfortable with crypto held by a regulated third-party custodian, and 85% were comfortable moving crypto into a separate account as part of the loan. Comfort did soften as the process got more operationally specific: 65% were comfortable if the process required securely transferring crypto on a separate platform. That gradient is the design brief in one line: every additional step of perceived complexity costs comfort, so the pledge experience has to be simple and well explained.

Hesitations were specific and addressable. The most common concerns were security and hacking (65%), losing access to their crypto (62%), and trusting the lender, platform, or custodian (52% each). And when we asked what would make a company offering this feel trustworthy, practical mechanics beat brand every time. A clear explanation of how the process works (62%) and strong security protections (50%) led, followed by assurance that their crypto remains theirs unless they default (38%), a qualified custodian (27%), and a clear explanation of what happens if crypto prices change (23%). A well-known crypto brand (17%) and a well-known lending brand (15%) ranked below every mechanical assurance.

Before they were ready to move forward, the single thing respondents most wanted explained was how their assets would be protected (55%), followed by who holds the crypto, what happens if they miss a payment, and what happens if prices change. When we tested descriptions of the product itself, the winner was "put your crypto to work without selling it" (33%), ahead of "unlock better borrowing terms with your crypto" (27%).

What this means if you run a lending book

Three takeaways travel directly from this research into a lender's roadmap.

The demand is already inside your funnel. These are not crypto tourists. They are prime-aged, financially established borrowers who recently applied for personal loans, auto loans, and mortgages, and who frequently walked away unhappy with the rate or amount. A collateral-enabled offer does not require finding a new audience; it re-engages applicants you already touch.

Lead with the rate. The clearest, most consistent driver of appeal was a lower interest rate, which a majority identified as the single most compelling benefit. Second-look approvals and down-payment support are powerful for specific segments, but broad positioning should lead with economic value.

Win on transparency, not logos. Comfort with custody and partnership was high out of the gate, and the deciding factor was a clear explanation of how the process works and how assets are protected. That is good news for a lender partnering with Vault: you do not need to be a crypto brand to be trusted here. You need a clean, well-explained process and a qualified custodian, both of which are built into Vault's program structure.

The bottom line

The strongest read from this study is not the 85% headline on its own; it is that within the exact population a collateral program would reach, the demand is real and specific. The people who would use this already own the assets, already borrow, and already tell us the current experience leaves rate and approval on the table. The barriers are the kind you clear with clarity rather than hype. If you are a lender and want to see what a collateral-enabled product would look like in your stack, we'd love to chat.

Frequently asked questions

How many people were surveyed, and who were they? The study was fielded in May 2026 by PinPoint Collective. It began with a screened pool of 600 US adults aged 25 to 50 with household income of $60,000 or more who were employed or in school. Within that pool, 388 (65%) owned digital assets, and 60 qualified respondents both owned crypto and had actively sought credit in the prior two years. Findings within the qualified group are directional and are not projectable to the general population.

Does 85% mean most borrowers want crypto-collateralized loans? No. It means that among crypto owners who had recently shopped for credit, 85% said they would consider the concept after reading it. That is the population a collateral-enabled or second-look offer would actually reach, which is why the signal is useful, but it is not a claim about all applicants.

How many US adults own digital assets overall? The Harris Poll's 2026 survey put national ownership at roughly one in four US adults. Within our screened, borrowing-relevant audience of younger, employed, higher-income adults, ownership was 65%, which is consistent with this demographic over-indexing on financial engagement.

Which benefit mattered most to borrowers? A lower interest rate. It was the top benefit before and after the concept was introduced, and 53% chose it as the single most compelling benefit, ahead of accessing funds without selling crypto (22%).

What did borrowers need in order to trust the product? Clear mechanics over brand. A clear explanation of how the process works (62%) and strong security protections (50%) outranked a well-known crypto brand (17%) or a well-known lending brand (15%). The thing respondents most wanted explained upfront was how their assets are protected (55%).

Are these borrowers comfortable moving crypto into custody? Largely, yes. Ninety percent were comfortable with crypto held by a regulated third-party custodian, 85% with moving assets into a separate account for the loan, and 82% had already moved crypto between wallets or accounts on their own.

See Vault inside your loan application

A 30-minute walkthrough of the pledge experience, reporting, and collateral return, with your loan products in mind.